Most people heading into retirement are thinking about everyday living, travel, family, and finally having more freedom with their time. What often gets less attention is healthcare. Yet over time, healthcare can become one of the biggest expenses in retirement and one of the fastest ways to put pressure on the assets you worked hard to build.

That is not meant to be alarming. It is simply practical. During your working years, much of healthcare is handled through an employer plan, with premiums coming out of a paycheck and many of the details staying in the background. Retirement changes that. Suddenly, healthcare becomes something you have to think through much more intentionally.

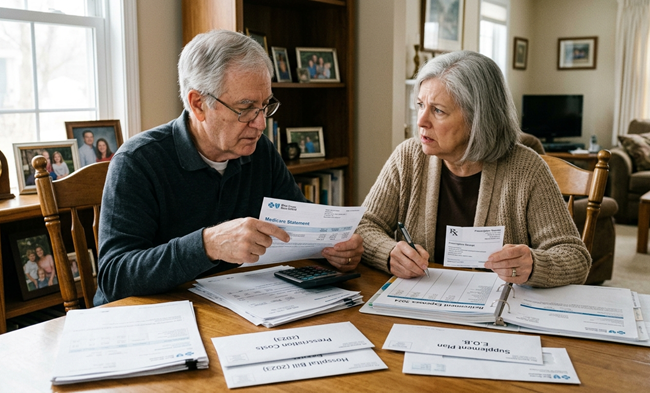

That is where the planning gap often begins. Many people assume Medicare will cover everything once they turn 65. It is an important foundation, but it is not all-inclusive. Premiums, deductibles, supplemental coverage, prescription costs, dental, vision, and other out-of-pocket expenses can all become part of the picture. If you retire before Medicare age, there can be an even bigger challenge in those transition years.

Many people also do not realize that the way income shows up in retirement can affect what they pay for Medicare, which is one more reason healthcare planning should be connected to tax and income planning. It’s all connected more than many realize.

For many households, this becomes one of the most underestimated expenses in retirement. Recent estimates suggest an average retired couple may spend around $330,000 on healthcare throughout retirement, and that figure does not include long-term care.

What makes this more important is that there is no one-size-fits-all answer. A healthy couple retiring at 67 will face a different healthcare strategy than someone stepping away from work at 62. A widow will look at these decisions differently than a married couple. A business owner may have different options than someone leaving a large employer plan. The right answer depends on timing, health, income, assets, taxes, and the kind of retirement you want to live.

That is why healthcare should never be treated as a side issue. It affects cash flow, withdrawal strategy, and the overall flexibility a household has in retirement. It may even affect what is ultimately left for a spouse or family. In real retirement planning, these decisions are connected.

A good financial planner talks about retirement through a panoramic view that includes income, taxes, investments, healthcare, and legacy. We have found that people gain more confidence when they stop looking at these decisions one at a time and start seeing how they work together. That is especially true with healthcare, because the costs may not arrive all at once, but they can shape a retirement plan over time.

Long-term care is part of that conversation too. It is not always comfortable to think about, but it is practical to address. Ignoring it does not make the risk go away. Thinking through it ahead of time can help preserve flexibility, protect assets, and create more peace of mind.

Keith Leverentz, NSSA®, is founder of The Life Group and has helped Tri-State area families and retirees since 2003 with personalized financial planning, investment guidance, and retirement strategies designed to bring greater peace of mind. You can visit their website at TheLifeGroupLLC.com.

Read Julien’s Journal, CHOICES For Fifty Plus and Tri-State Home TRENDS from the Comfort of Your Home!

Click Here or call 563.557.7571 to subscribe for convenient delivery to your home or business by mail of all three magazines for one low subscription price.

Comment here